How to Save Tax Legally in India?

A tax is a good duty, but a tax higher than necessary is not. Most people in India lack the knowledge to reduce their tax burden. When done properly, anyone can reduce their taxes without violating any laws.

This article describes how taxes can be dealt with practically and legally in a better way. It focuses on tax-saving tips in India, typical income tax deductions, and strategic financial planning.

Table of Contents

The Importance of Tax Planning

Tax planning is not merely about saving money by the end of the financial year. It is about making sure you make financially sound decisions year-round. Correctly carried out, tax planning in India assists people:

- Reduce overall tax liability

- Build long-term wealth

- Improve financial discipline

- Avoid last-minute stress

In March, many individuals rush out to buy investments at random to get a tax deduction. The latter strategy is prone to making bad decisions. A budgeted approach is more effective and provides insight into where the money should be used.

How to Figure Your Taxable Income

One should understand how taxable income is computed before considering how to save on taxes.

Taxable income includes:

- Salary or wages

- Business or freelance revenues

- Rental income

- Interest earned on savings as a fixed deposit

Once you have determined the total income, you may obtain eligible income tax deductions. It is the rest that you pay tax on. Being aware of this organization is conducive to some planning and disentangling in the future.

Key Tax Saving Tips in India You Should Know

It has a few easy steps that one can take in order to minimize their taxes. Here are some helpful tax-saving tips in India that apply to most taxpayers.

Start Early in the Financial Year

Early planning is more viable and helps avoid haste, rather than investing in March, spread out the yearly investments.

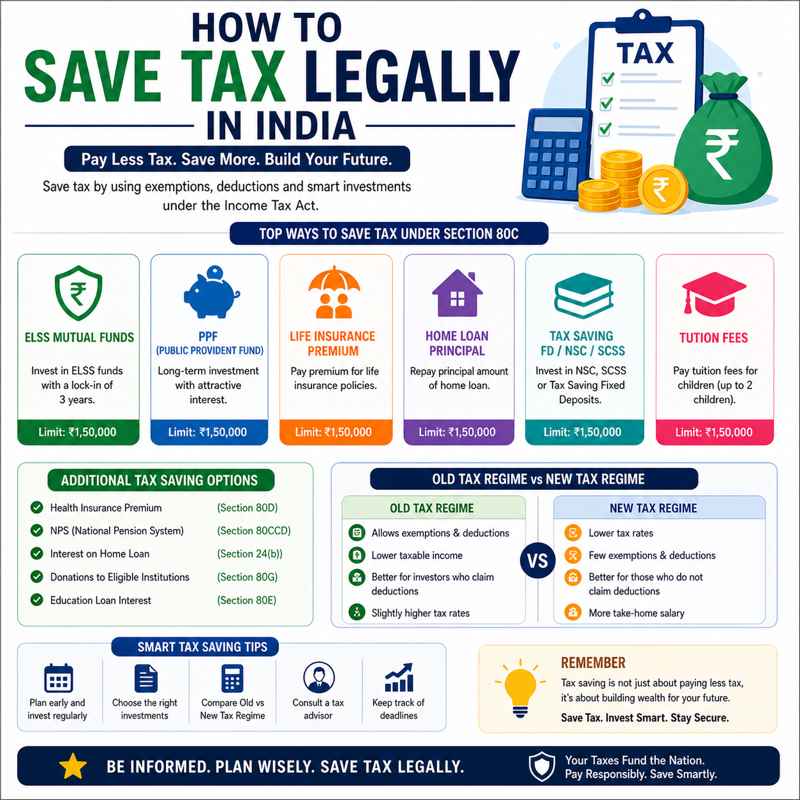

Select the Appropriate Tax Regime

There are two tax regimes in India:

- Old Regime (with deductions)

- New regime (lower rates, fewer deductions)

Compare and compare before filing. The former may be more advantageous for those with various income tax breaks.

Keep Proper Records

Keep records of such items as:

- Investment proofs

- Rent receipts

- Medical bills

They are useful in getting deductions and avoiding problems in the future.

Section 80C Benefits Explained

Section 80C benefits are one of the most well-liked methods of cutting down on tax. Under this section, one can deduct (upto) ₹1.5 lakh per year.

Typical investments under Section 80C

- This is associated with the Public Provident Fund (PPF)

- The Ministry of Labor introduced the Employee Provident Fund (EPF)

- Equity Linked Savings Scheme (ELSS)

- Life insurance premiums

- National Savings Certificate (NSC)

Such options not only help save more on taxes but also help achieve long-term savings.

Why Section 80C Matters the Most

Section 80C benefits are popular because they are easy to understand and offer a safe investment opportunity. This would be the first step towards tax planning in India and would form the foundation of the annual investment plan for many salaried employees.

Other Important Income Tax Deductions

In addition to Section 80C, several other tax deductions can help you save tax in India.

Health insurance is provided under this section 80D

You are allowed deductions for health insurance premiums:

- ₹25,000 for self and family

- Additional ₹25,000 for parents (₹50,000 if senior citizens)

This will motivate individuals to obtain insurance and minimize tax liabilities.

Section 24 Home Loan Interest

If you have a home loan, the interest you pay is deductible up to ₹2 lakh per year.

Section 80E – Education Loan

The interest incurred on education loans can be fully deductible for a certain period.

Section 80G – Donations

Gifts to charities that are allowed are deductible. This not only benefits society but also your tax savings.

Wise Decisions on making Investments for Tax Savings

Investments are important in tax planning in India. Making the right decisions can make you rich and help you pay less taxes.

Popular Investments that are Tax-Saving

- EELS Mutual funds (market-linked returns)

- PPF (safe and long-term)

- Tax-saving fixed deposits

- The US retirement plan is known as the National Pension System (NPS)

The options will have varying levels of risk and lock- ins. Choose based on your interests and financial well-being.

Salary Structuring to Improve Tax Savings

Significant taxes can also be reduced by being clever with employee salary structures.

Common Components That Help Save Tax

- House Rent Allowance (HRA)

- Leave Travel Allowance (LTA)

- Meal coupons

- Telephone and internet credits, refunds

These elements reduce taxable income under the law and result in a higher take-home salary.

Tax-Saving Tips for Salaried People in India

Salaried people are quite reliant on their employers regarding tax assistance. Nevertheless, they can take other actions independently.

Practical Steps

- List investments with your employer

- Take all the deductions from the income tax

- Review Form 16 carefully

- Regularly invest in tax-saving schemes

By these steps, getting your tax saved India without complications and maintaining your records will be simpler.

Tax Planning in India for the Self-Employed

Professionals who are self-employed and proprietors have different tax obligations. They should keep good records and a plan.

The most important aspects to be taken into consideration

- All business costs are tracked

- Take deductions on renting the office, traveling, and utility expenses

- Presumptive taxation to be used where allowed

- PGS Investments are eligible under Section 80C

When plans are well laid out, there is little likelihood of breaking the law, and taxes bear the burden.

Mistakes to Avoid While Trying to Save Tax

Consulting tax saving tips in India; however, the number of individuals committing unnecessary mistakes is great.

Common Mistakes

- Investing only for tax savings rather than returns

- Ignoring documentation

- Missing deadlines

- Failure to provide a comparison of the tax regimes

Such errors can be avoided to improve overall financial condition and prevent unnecessary losses.

How to Build a Year-Round Tax Plan

Tax savings are not a one-off event. An annual program is more effective.

Planning Things to do

- Have financial targets at the beginning of the year

- Allocate funds for Investments monthly

- See progress on tax savings quarterly

- Modify strategy, as appropriate

This method makes tax planning in India easy and stress-free and helps you keep your finances in check.

Expert Advice for Better Tax Management

Finance experts recommend targeting both tax savings and long-term growth. It is also important to save tax, and it should not be the objective.

Balanced Approach

- Use a combination of tax-saving investments and growth choices

- Store an emergency amount separately

- Do Not Keep All the Money in Lengthy Arrangements

- Review investments yearly

The tax-saving mechanisms in India can help such individuals save on taxes and accumulate wealth in the long run.

Final Thoughts

It is not too hard to legally save on taxes when you are aware of the options available. Knowing the deductions for income tax and intelligently leveraging Section 80C benefits, people can save a lot of tax.

It is all a matter of consistency. There are simple tax-saving tips in India that can help improve financial performance year-round. Everyone can enjoy good tax planning in India and good financial planning, whether they are an employee or a self-employed worker.

Frequently Asked Questions (FAQs)

How is it best to save tax in India?

Save tax in India is best accomplished by offering an option for section 80C benefits, such as PPF, EPF, and ELSS, alongside other income tax deductions like health insurance and home loan interest.

Is it possible to use both the old and the new tax regimes together?

No, you will have to select one regime in a financial year. You should compare before deciding to help you save tax in India more effectively.

Is tax planning only for high income individuals?

No, tax planning is beneficial to everyone. Tax-saving tips: India can save a lot with seemingly small amounts of money.

At what point should I start tax planning in India?

The most usual way is to begin the financial year. Planning early gives more time to enjoy tax deductions on income taxes and make better financial decisions.